Robert Sutton, Executive Vice President of Innovation at BNSF Logistics, reviews how month-over-month market and economic factors affect transportation and the supply chain.

BUSINESSES STILL HAVE A BIG APPETITE FOR LABOR

Employment rose in health care, hotels and restaurants, retail, manufacturing, finance, and wholesale trade.

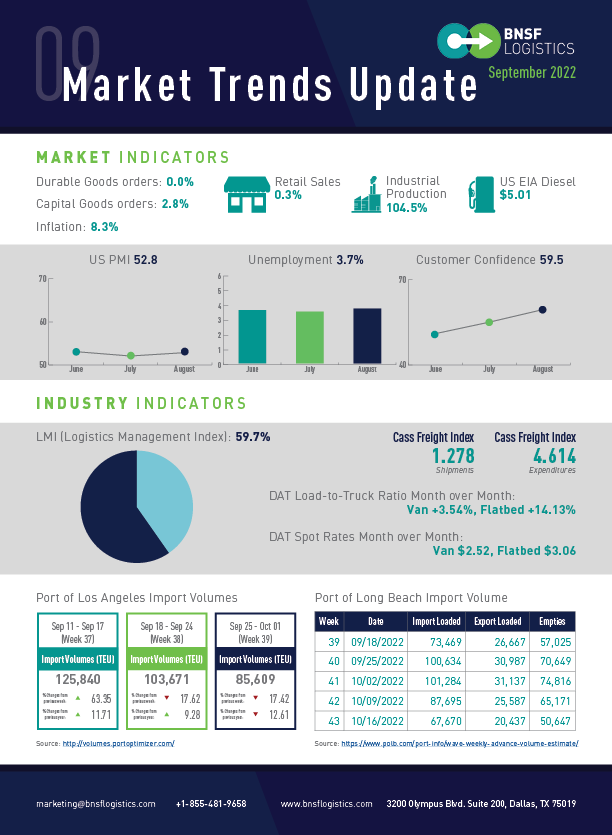

- The unemployment rate rose to 3.7% from 3.5% (six months high)

- The U.S. added a robust 315,000 new jobs in August.

- Professional businesses added 68,000 employees.

- Labor force participation rate increased to 62.4% from 62.1%.

Overall, in the last couple of months, the annual inflation rate has dropped, which is heading in the right direction; it should be noted that the decline in the headline rate is essentially a function of declining energy prices.

- The U.S. inflation rate is 8.3%, a decline from last month, but includes a rise in the core inflation rate.

- Gasoline prices fell by 10.6%.

- The consumer sentiment index is 59.5 in September, up from 58.2 in August.

The money Americans are spending is still high, but it reflects the higher prices they are paying because of inflation. Adjusted for inflation, retail spending has been flat for the past year.

- Sales rose by 0.3%.

- Auto and parts sales rose 2.8%.

Economic data reflecting the housing market conditions have been weak, as seen by the drop in permits signaling weakness in future projects.

- New U.S. homes construction rose 12.2% in August.

- Building permits for new homes fell 10%.

Inventory continues to be the main impediment to increasing new-vehicle sales volumes above the rates seen in recent months. The higher prices, reduced incentives, and rising interest rates also push average monthly payments higher.

- The seasonally adjusted annual rate of new vehicle sales is 13.2 million units.

- The average transaction price for August 2022 should reach $46,259.

Manufacturers feel the brunt of rising interest rates and high inflation as customers scale back. And they are also confronting ongoing shortages of supplies and labor that have hindered production for the past year and a half.

- Durable goods orders were flat in July.

- Core orders increased by 0.4%, excluding transportation and government.

- Orders for new passenger planes jumped 14.5% in July.

SENTIMENT REMAINED OPTIMISTIC REGARDING DEMAND

This is the second month in a row the PMI was at its lowest since June of 2020, showing a continued slowing in the growth rate in manufacturing.

- August Manufacturing PMI® was flat from July at 52.8%.

- 27th month in a row for expansion.

- Electronics: “Demand from customers is still strong.”

- Machinery: “Continue to struggle with electronic component shortages.”

- Primary Metals: “Demand is softening.”

- Plastics: “Orders are still strong through the end of the year.”

The logistics industry continues to expand, driven primarily by high inventory levels and associated costs.

- LMI fell in August to 59.7, the first reading below 60 since May 2020.

- Transportation capacity is at 64.3.

- Warehouse capacity is at 42.3.

The spread between the two capacity metrics is 22.0, the second-highest reading over the last four years. The only other time we saw a similar distance was April 2019, when the two metrics were 21.3 points apart.

The shipments component of the Cass Freight Index® rose 3.6% on a y/y basis in August. Ahead of the revised 1.9% y/y increase in July.

- On a seasonally adjusted (SA) basis, shipments rose 5.5% m/m in August.

The expenditures component of the Cass Freight Index® rose 1.9% m/m in August after a 3.0% decline in July, with shipments up 6.6% and rates down 4.4%.

- The Cass Expenditures Index was still 20% higher than year-ago levels in August, decelerating from 29% in July.

- On an SA basis, expenditures rose 2.1% m/m in August, with shipments up 5.5% m/m and rates down 3.2%.

Preliminary Class 8 orders for August jumped. Most OEMs began placing a limited number of orders for the first quarter of 2023.

- Class 8 orders for August 21,400 units.

- S. trailer orders in August jumped compared with a year earlier but were still tepid at 17,700.

The bottom line is that the need for carriers to replenish their fleets is still much higher than the current production capacity under the current restrictions. Even as the economy has slowed, the need for replacements will continue to push demand which will not be able to be fulfilled entirely until supply chain shortages are resolved.