Robert Sutton, Executive Vice President of Innovation at BNSF Logistics, reviews how month-over-month market and economic factors affect transportation and the supply chain.

LABOR PARTICIPATION REMAINED STABLE, WITH EDUCATION AND HEALTH GAINS

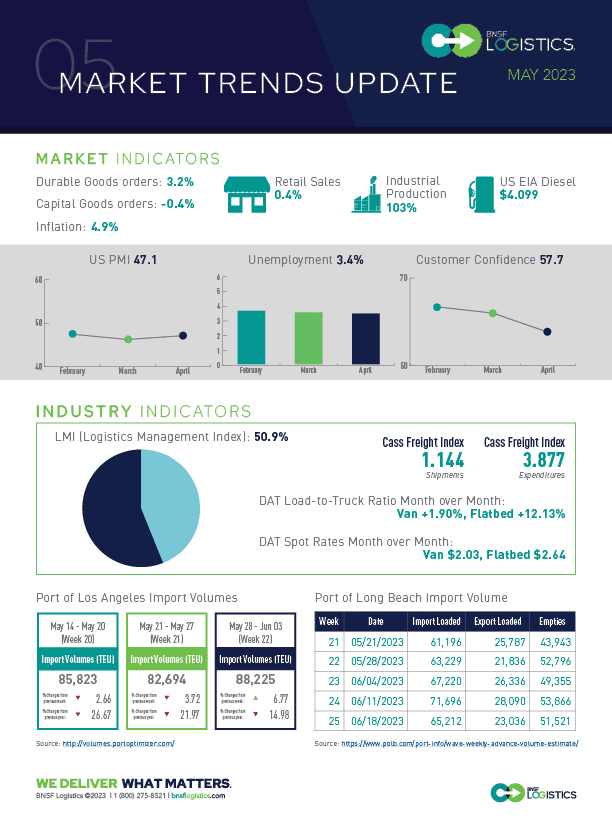

The US economy added 253,000 jobs in April, up from 165K in April. As a result, the unemployment rate fell from 3.5% to 3.4%.

– Labor participation was flat at 62.6%

– Education and health saw the most significant gains, adding 77K jobs

– Largest gains were in education and health – 77K

– Job openings fell by 340K at the end of March to 9.6 million, which is the lowest level since May 2021

The Consumer Price Index (CPI) rose 0.4% in April, while core inflation increased 0.4% during the same period. Consumer confidence also decreased from 104.0 to 101.3, with the Present Situation Index rising from 148.9 to 151.1, and the Expectations Index fell from 74.0 to 68.1.

– Used car prices and gasoline also were up in April.

– Rents were up 0.1%, and prices of used vehicles increased.

The retail industry rebounded slightly, with sales increasing by 0.4% in April after falling for two months.

– Sales of new vehicles and parts increased by 0.6% in April

– Sales at gas stations dropped by 0.8%

The housing market saw a setback in April, with new home starts increasing by 2.2%. In addition, building permits for new homes dropped by 1.5%, indicating a continued downward trend.

– Single-family construction increased by 1.6%, while multi-family dropped by 5.2%

– Building permits for single-family rose by 3.1%, while multi-family fell by 9.7%

New orders improved in March by 3.2%, but orders for passenger planes drove this. As a result, orders net of transportation activity only rose by 0.3% – positive but not exactly something to celebrate as the sector remains under pressure.

– Orders are 4.8% higher than in the same period last year

– Business investment decreased to 2.0%, which is the lowest reading since 2020

PMI CONTINUES TO SHOW CONTRACTION WHILE LMI IS IN DECLINE DUE TO INVENTORY LEVELS.

April Manufacturing PMI® increased to 47.1 percent, signaling the fifth month of contraction after two and a half years of expansion.

– New Orders contracted at a slower pace. New Export Orders is still in contraction territory but are improving. Customers’ Inventories are entering the low end of “too high,” which puts downward pressure on future orders.

– Output/Consumption, including Production and Employment, was positive with a combined 4.4-percentage point downward impact on the PMI® calculation.

– Supplier Deliveries indicate faster deliveries, while Inventories dropped further into contraction.

LMI was 50.9 in April – down 0.2 points from March. This is the index’s lowest reading since its inception 6.5 years ago, led by the decline in Inventory Levels.

– Transportation Capacity was 70.6 in April, up 0.8 points from last month.

– Transportation Utilization increased by 5 points to 55.0 in April

– Inventory Levels 50.9 which was down 4.7 points from March

Inventory Costs were down 0.9 points from the prior month and 87.7 points from last April. Warehousing Capacity was down 3.5 points from last month, and the future index was 57.0. Warehousing Prices were down 2 points from the prior month but still in elevated expansion territory. Future index was 61.9.

In April, the Cass Freight Index fell 1.3% m/m for shipments, following a sizable 3.8% m/m drop in March. And normal seasonality suggests the y/y may worsen over the next few months.

– The expenditures component of the Cass Freight Index fell 2.1% m/m in April

– Inferred Freight Rates declined 11.9% y/y after an 8.3% decline in March.

Preliminary Class 8 net orders for April declined 37% sequentially and are 20% below last April. The weak activity levels in April were expected, but it is happening sooner than usual due to build slots already being filled for 2023. As a result, expect order levels to remain muted throughout the summer.