Robert Sutton, Executive Vice President of Innovation at BNSF Logistics, reviews how month-over-month market and economic factors affect transportation and the supply chain.

THE ECONOMY IS STILL GOING STRONG DESPITE CONCERNS

The labor market and broader economy keep going strong despite concerns about a more general economic slowdown driven by the Fed’s effort to slow demand through interest rate hikes.

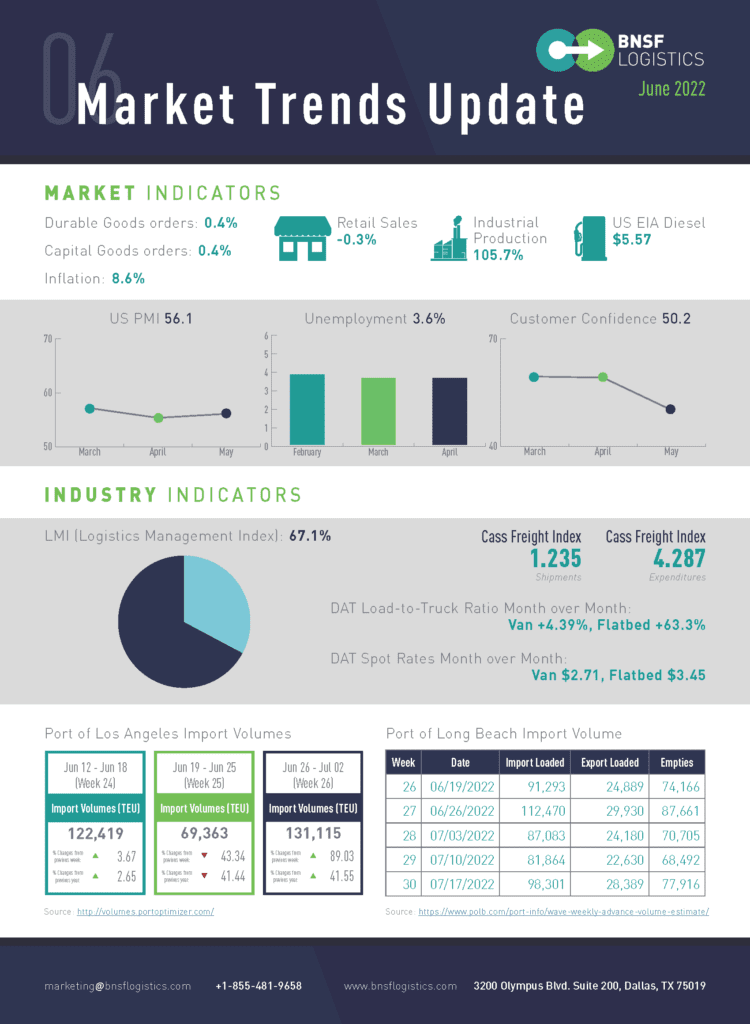

- The U.S. added 390,000 new jobs in May.

- The unemployment rate was unchanged at 3.6%.

- Restaurants and hotels led in hiring, adding 84,000 jobs.

- The labor participation rate is up to 62.3%.

The surge in inflation has shown little sign of cresting. Gas prices have jumped again to record highs. Food costs keep climbing. And rents have also risen sharply. Prices are likely to show another significant increase in June.

- The cost of living jumped 1% in May.

- U.S. inflation is 8.6% (a 40-year record).

- The price of gasoline was up 4.1% in May.

Rising prices due to high inflation are also discouraging shoppers, especially as discretionary income continues to be squeezed. Americans are shifting their spending toward services such as travel and entertainment.

- Sales at retailers were down 0.3% in May.

- Auto and parts sales fell 4% last month.

The trend in single-family starts is downward as higher mortgage interest rates will likely slow demand, and the movement is expected to persist through the year’s balance.

- Construction starts down 14.4% in May.

- Demand for houses also fell by 7%.

- Single-family homes fell 9.2%, while apartment starts down 26.8% last month.

The industry remains in a demand-driven, but supply-constrained environment as manufacturers continue to struggle to secure sufficient microchips to increase production.

- Auto sales fell to 12.7 million from 14.3 million.

- Inventory at dealerships was around 1.13 million units this month.

- Consumers are looking for fuel-efficient, smaller vehicles (including hybrids).

- The average list price rose to $45,495.

Factories are working at full tilt to meet strong customer demand, and business investment is robust, but high inflation and industry 4.0 technologies rising interest rates are starting to cause erosion. Ongoing supply shortages are also a hindrance.

- Durable goods orders at U.S. factories were up 0.4% in April.

- Orders for commercial planes climbed 4.3% in April.

- Autos orders slipped 0.2%.

- Capital goods orders increased 0.4% for the month.

THE OVERALL ECONOMY KEEPS EXPANDING FOR THE 24TH MONTH IN A ROW.

After a contraction in April and May 2020, the economy kept its upward trend for the last two years.

- The May Manufacturing PMI® registered 56.1%.

- Plus 0.7% from the previous month.

- Demand expanded.

- Customers’ inventories remain at a very low level.

- Backlog of Orders Index increasing.

All the six biggest manufacturing industries — Machinery; Computer & Electronic Products; Food, Beverage & Tobacco Products; Transportation Equipment; Petroleum & Coal Products; and Chemical Products — registered moderate-to-strong growth in May.

The logistics industry continues its regression after nearly two years of rapid growth.

- The Logistics Management Index in May fell to 67.1.

- Transportation Capacity is up 7.8.

- Transportation price is down 8.7.

Despite this slowdown, it should be noted that we are still observing a healthy rate of growth in transportation, but one that pales in comparison to the unsustainable growth rates observed in 2021.

The shipments component of the Cass Freight Index® rose 5.4% m/m in May (up 4.0% SA), more than recovering the 2.6% decline in April. Normal seasonality from here would have the shipments component back up 2% y/y in June and flat to up 1% for 2022. The news from the retail sector and the oil markets suggests it’s probably optimistic, but at this point, it’s a pretty stable environment—no significant downturn.

The expenditures component of the Cass Freight Index fell 4.9% m/m in May, with shipments up 5.4% and rates down 9.8%. The freight rates embedded in the two components of the Cass Freight Index still rose 31% y/y in May, in line with April, despite a 9.8% m/m decline.

Demand for new trucks remains healthy. Freight is growing, and fleets need more trucks to meet customer demands and trade in older vehicles.

- Class 8 truck orders dropped in May by 13% and 48% for the year.

The supply of new trucks has been running way behind the demand for over a year now, and many fleets need to catch up to their replacement cycles.