Robert Sutton, Executive Vice President of Innovation at BNSF Logistics, reviews how month-over-month market and economic factors affect transportation and the supply chain.

U.S. JOBS INCREASED IN DECEMBER, AND RETAIL SALES SHOWED MIXED RESULTS

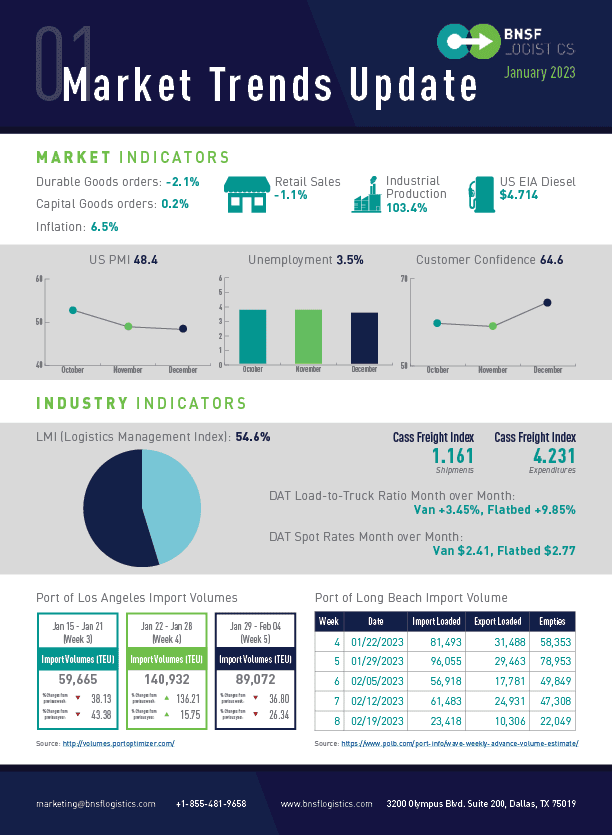

December saw a slight slowing of job growth, with only 223,000 new jobs added, the smallest gain in two years. Despite this, the unemployment rate dropped slightly from 3.6% to 3.5%, matching pre-pandemic levels.

– The labor participation rate increased slightly from 62.2 to 62.3

– Hourly pay rose modestly by 0.3% last month

– Wages have increased by 4.6% over the past year

– It will take 2.5 million people entering the labor force to achieve pre-pandemic levels

The overall costs of goods and services dropped by 0.1% in December, resulting in an annualized rate of 6.5%. This marks a 28% decline since June, when the rate peaked at 9.1%, and is a step closer to the 2% to 3% level that the Federal Reserve is aiming for.

– The core rate rose by 0.3% sequentially, but the annualized rate still declined to 5.7%

– Gasoline prices were the main driver of the decline

Recent retail sales figures show a 1.1% decline in December, mainly due to falling gasoline prices and fewer purchases of new cars. This signals a continued slowdown in overall economic activity as consumers shift their spending to services such as travel and recreation.

– Retail sales declined in almost every major retail category

– Overall retail spending has increased by 6% in the past year

Building permits fell in December, indicating that the market has not fully recovered from the pandemic.

– New home construction fell to a seasonally adjusted 1.38 million in December

– Building permits for new homes also fell 1.6% to 1.33 million in December

Auto sales rose this month. However, the annualized volume was the lowest since 2011. Despite the slowing economy and higher interest rates, analysts expect 2023 sales to increase.

– Auto sales rose 7.3 percent in December 2022 to 1.28 million

– The annualized volume was 13.3 million

November durable goods orders fell, indicating a weakening economic activity due to consumer buying patterns, higher interest rates, and a slowing global economy. In addition, as supply chains shrink, transport costs are falling.

– Durable goods orders overall decreased by 2.1% in November

– Most of the decline was attributed to a 36% drop in airplane orders

– New orders excluding transportation activity rose 0.2%

– Higher interest rates and a fading global economy have caused a slowdown in business investment, which posted a 0.2% increase last month but an annual growth rate of 5.7%

PMI® AND LMI INCREASED IN DECEMBER DESPITE DECLINING IN TRANSPORTATION

The October Manufacturing PMI® shows that the manufacturing sector is again contracting after a brief period of expansion.

– The October Manufacturing PMI® registered 48.4 percent, 0.6 points lower than in November

– The sector is showing contraction for the 2nd consecutive month after the expansion that started in June 2020

– Transport equipment: Original equipment orders are slowing

– Chemical: Demand remains low. Demand is down despite a promising 2023 pipeline

– Machinery: Customers are delaying capital purchases due to economic uncertainty

December showed mixed results for the LMI, with an increase in some metrics and a decrease in others.

– The Logistics Management Index (LMI) was up 1 point in December, the first increase in eight months

– Transportation Capacity registered 69.5 in December 2022, a 1.9-point decline from November

– Inventory Levels rose 2.5 points from November but are 4.3 points lower than last year’s

Overall, these results suggest that the logistics industry is still in a state of flux, but there are signs of improvement. With more months of data, the industry can continue to monitor these trends and adjust accordingly.

The Cass Freight Index for December showed a decline in shipments on a year-over-year basis. This indicates that freight demand remains resilient but soft.

– Shipments fell 3.9% y/y in December

– Month-on-month performance was boosted by seasonality to a 1.2% gain on a SA basis, reflecting resilient yet soft freight demand

December saw a decline in Cass Freight Index Expenditures. This decline was a continuation of the trend seen in November.

– Expenditures fell 4.3% year-on-year and 5.5% month-on-month

– On an SA basis, expenditures fell 4.2% month-on-month

The Class 8 and Trailer markets have seen strong demand throughout 2022 despite economic and financial uncertainties, with order levels reaching their second highest of the year in November

– Preliminary Class 8 net orders for December fell by 21% from the previous month to 28,300 units

– Trailer orders reached 39,000 in November, down slightly from the 44K last month

Fleets fill orders as soon as build slots become available. As fleets replace outdated equipment, demand should remain strong through the first half of next year.